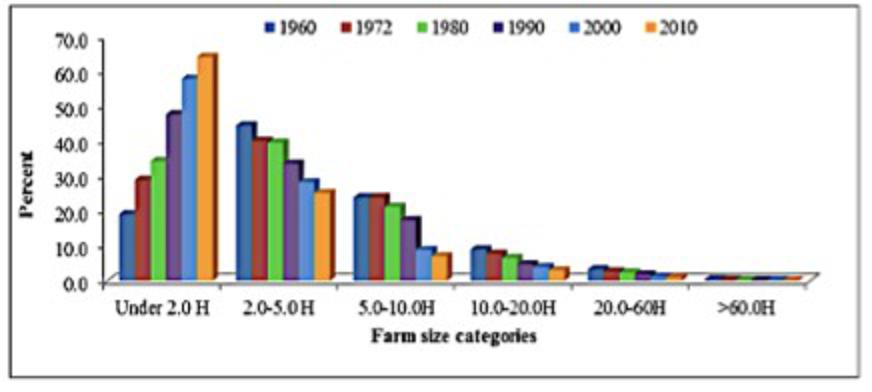

Small & marginalized farmers represent a major portion of farming households in Punjab. It includes farmers with landholding up to 12.5 acres and landless farmers with no collateral to offer to the formal lending institutions. Out of the total operational farms, only 19% was under 5 acres as reported in the Agriculture Census, 1960. This increased to a staggering 67% in the 2010 Census. More interestingly, with an average number of 2.6 fragments in each farm, the average size of farms in this category of under 5 acres is about 2.5 acres. More than 60% of Pakistan’s population either reside or belong to rural areas as reported by the Government of Pakistan. Punjab being the largest province accounts for 60% of the total population, is home to the highest absolute number of poor people with an estimated poverty rate as high as 42.6%. Beyond just small size, these poor farms see high levels of illiteracy, and a lack of access to credit and better markets, which become critical constraints to the adoption of technology. Thus, most such farmers cannot take risks associated with modernization and make a move to high-value crops.

The linkage between the formal financial sector and farmers ranged from poor to completely absent depending on farm size and education level of the farmer, among few other factors. Commercial banks seem reluctant in extending the low-cost loan due to challenges in the realization of agricultural land and high operational cost for small size loans. Even the segmented farmers are not motivated to approach commercial banks due to lack of collateral, difficult documentation, and lengthy procedural requirements. On the other hand, the formal credit available to the small and marginalized farming community with increased land fragmentation is only from the micro-finance institutions/banks which again is of high cost ranging from 25% to 35%. In absence of formal lending, the farmers relied on high-cost informal and formal sources of credit, which mostly means getting loans from Arti (commission agent). Loans from Arti bounds farmers to less than fair terms and conditions and often farmers suffer at the hands of the Arti at the time of sale of their produce and end up earning unfair and low margins. As a result, these small farmers had to bear the financial burden of agriculture production, thus trapping them in a perpetual cycle of poverty due to low margins and limited income.

To reduce farmers’ financial burden and in turn help improve the quality of their lives, the Government of Punjab, developed a digitized solution for the provision of easy, hassle-free, and low-cost formal agriculture credit. “Empowerment of Kissan Through Digital & Financial Inclusion” (e-Credits) is an innovative program developed by Agriculture Department Punjab. The program facilitates the small & marginalized farmers of Punjab with the provision of interest-free digital formal credit to enhance their yields per acre and increase the overall financial inclusion in the country. Most of the complex functions including registration, collateralization, and disbursement of the loan were automated. It was ensured that disbursement was made through a basic bank account which enabled these farmers to be part of the formal financial sector. It is a five-year program providing interest-free agriculture credit for the newly registered farmers in years 1 & 2. Whereas, a nominal 4%, 8%, and 12% low-cost markup interest were charged for years 3, 4 & 5 respectively. All of the loans are given to farmers having landholding of fewer than 12.5 acres for Rabi and Kharif crops. It is a breakthrough for the small and marginalized farmers that the program has enabled formal low-cost lending.

So far, over 850,000 loans are disbursed of over rupees 61 billion by five partner banks in two crop cycles of Rabi & Kharif. For the first time in the history of Pakistan, a substantial chunk of these formal loans went to landless farmers. These farmers were included in the program through a group lending mechanism and secured via social guarantees while also benefiting from being part of the formal financial sector. Excitingly, a minor portion of these interest and hassle-free loans comprised of female farmers. As reported in the project steering committee 93% of the farmers were new-to-bank. Remarkably, the recovery rate reported by partnering lending institutions remained 99%. Being part of the formal financial sector enable these farmers to develop a sense of formal savings, credit, remittance, payment, and insurance.

The introduction of the E-credit scheme has benefitted the economy as a whole, through an increase in the GDP contributed through agriculture. Programs like e-Credits play a major role in facilitating Pakistan’s FATF rating by bringing the unbanked to the formal sector. This has been an excellent tool especially in rural areas such as Kasur, Rajanpur, Rahim Yar Khan, and Dera Ghazi Khan where a massive number of farmers took loans in both the cropping seasons. These new-to-bank farmers have learned how to work with financial institutions and avail banking services like deposit and withdrawal. The new and optimized digital process for the mutation will prove to be a game-changer for the agriculture sector loans, significantly reducing the time taken in the traditional process of collateralization and the high cost associated with it. Exploitation from the Arti’s and the high-cost formal sector has shown us the limits to the security of these small and marginalized farmers. There is a need to support such interventions through allocation and disbursal of more and timely funds while upscaling e-Credits to national levels facilitating small and marginalized farmers of Pakistan.

By Muhammed Mus-haf Khan, the writer is a certified expert on financial inclusion from the Fletcher School of Law & Diplomacy, USA working with the Government of Punjab and can be reached on Facebook and Twitter accounts @MushafKhanPak.

- Empowering the Marginalized Kissan’s of Punjab through Digital Financial Inclusion - 10/05/2021

- Pakistan’s Agriculture & Climate Disaster - 09/04/2021

- Missing Pens! - 15/08/2020

{kind=link}